pandas

url_titanic = "https://gist.githubusercontent.com/butuzov/ed1c7f8f3affe6dd005c1ee40dc3f7f2/raw/87c7d72e009f1965263edc3431adbd4fab69f387/titanic.csv"

url_economics = "https://gist.githubusercontent.com/butuzov/ed1c7f8f3affe6dd005c1ee40dc3f7f2/raw/87c7d72e009f1965263edc3431adbd4fab69f387/economics.csv"

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

# Just So we can log

# nice logging

from icecream import ic

import sys, re

def printError(e): print("Error: {}".format(e), file=sys.stderr)

def jupyter(*args):

print(*[re.sub(r",\s{1,}", ", ", i.replace(",\n", ", ")) for i in args], file=sys.stdout)

ic.configureOutput(prefix='ic> ', outputFunction=jupyter)

rnd = np.random.RandomState(42)

Pandas

Talks:

Docks:

Books:

#Getting Started

pandas allow us plot, explore, data. perform math on large sets of it.

#Versions and general overview

# version

ic(pd.__version__)

> ic> pd.__version__: '1.5.3'

result >>> '1.5.3'

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

#Options

https://pandas.pydata.org/pandas-docs/stable/user_guide/options.html#available-options

ic(pd.describe_option("display.max_rows"))

with pd.option_context('display.max_rows', 2):

ic(pd.get_option("display.max_rows"))

ic(pd.get_option("display.max_rows"))

print("----"*20)

ic(pd.get_option("display.max_rows"))

ic(pd.set_option("display.max_rows", 2))

ic(pd.get_option("display.max_rows"))

print("----"*20)

ic(pd.reset_option("display.max_rows"))

ic(pd.get_option("display.max_rows"))

> display.max_rows : int

> If max_rows is exceeded, switch to truncate view. Depending on

> `large_repr`, objects are either centrally truncated or printed as

> a summary view. 'None' value means unlimited.

>

> In case python/IPython is running in a terminal and `large_repr`

> equals 'truncate' this can be set to 0 and pandas will auto-detect

> the height of the terminal and print a truncated object which fits

> the screen height. The IPython notebook, IPython qtconsole, or

> IDLE do not run in a terminal and hence it is not possible to do

> correct auto-detection.

> [default: 60] [currently: 60]

> ic> pd.describe_option("display.max_rows"): None

> ic> pd.get_option("display.max_rows"): 2

> ic> pd.get_option("display.max_rows"): 60

> --------------------------------------------------------------------------------

> ic> pd.get_option("display.max_rows"): 60

> ic> pd.set_option("display.max_rows", 2): None

> ic> pd.get_option("display.max_rows"): 2

> --------------------------------------------------------------------------------

> ic> pd.reset_option("display.max_rows"): None

> ic> pd.get_option("display.max_rows"): 60

result >>> 60

#DataTypes: Series and DataFrames

Types:

np.bool (bool) - Stored as a single byte.np.int (int) - Defaulted to 64 bits, Unsigned ints is alaso available (np.uint)np.float (float) - Defaulted to 64 bits.np.complex (complex) - Rarely seen in DAnp.object (O, object) - Typically strings but is a catch- all for columns with multiple different types or other Python objects (tuples, lists, dicts, and so on).np.datetime64, pd.Timestamp (datetime64) - Specific moment in time with nanosecond precision.np.timedelta64,pd.Timedelta (timedelta64) - An amount of time, from days to nanoseconds.pd.Categorical (Categorical) - Specific only to pandas. Useful for object columns with relatively few unique values.

ic(economics.dtypes.value_counts())

print("-"*60)

ic(economics.dtypes)

> ic> economics.dtypes.value_counts(): float64 3

> int64 2

> dtype: int64

> ------------------------------------------------------------

> ic> economics.dtypes: pce float64

> pop int64

> psavert float64

> uempmed float64

> unemploy int64

> dtype: object

result >>> pce float64

result >>> pop int64

result >>> psavert float64

result >>> uempmed float64

result >>> unemploy int64

result >>> dtype: object

#pd.Series

numpy array with labels

rnd_series = pd.Series(rnd.randint(0, 10, 6))

ic(type(rnd_series))

ic(rnd_series.shape)

ic(rnd_series.index)

ic(rnd_series.value_counts(normalize=True))

ic(rnd_series.hasnans)

> ic> type(rnd_series): <class 'pandas.core.series.Series'>

> ic> rnd_series.shape: (6,)

> ic> rnd_series.index: RangeIndex(start=0, stop=6, step=1)

> ic> rnd_series.value_counts(normalize=True): 6 0.333333

> 3 0.166667

> 7 0.166667

> 4 0.166667

> 9 0.166667

> dtype: float64

> ic> rnd_series.hasnans: False

result >>> False

#pd.DataFrame

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

# row

ic(economics.values[0])

ic(type(economics.values))

ic(economics.shape)

ic(economics.columns[0:4])

ic(economics.index[0])

> ic> economics.values[0]: array([5.07400e+02, 1.98712e+05, 1.25000e+01, 4.50000e+00, 2.94400e+03])

> ic> type(economics.values): <class 'numpy.ndarray'>

> ic> economics.shape: (574, 5)

> ic> economics.columns[0:4]: Index(['pce', 'pop', 'psavert', 'uempmed'], dtype='object')

> ic> economics.index[0]: Timestamp('1967-07-01 00:00:00')

result >>> Timestamp('1967-07-01 00:00:00')

economics.info()

> <class 'pandas.core.frame.DataFrame'>

> DatetimeIndex: 574 entries, 1967-07-01 to 2015-04-01

> Data columns (total 5 columns):

> # Column Non-Null Count Dtype

> --- ------ -------------- -----

> 0 pce 574 non-null float64

> 1 pop 574 non-null int64

> 2 psavert 574 non-null float64

> 3 uempmed 574 non-null float64

> 4 unemploy 574 non-null int64

> dtypes: float64(3), int64(2)

> memory usage: 26.9 KB

#Data: Generate Data (numpy)

pandas use numpy to generate indexes, and perform operations on matrixes

#Random data in Dataframe/Series

# generating random data based on numpy generated array

pd.DataFrame(rnd.randint(0, 10, 6).reshape(-1, 6)).head()

|

0 |

1 |

2 |

3 |

4 |

5 |

| 0 |

2 |

6 |

7 |

4 |

3 |

7 |

#Data: Import and Export

#Import

We can import data from: csv, excel, excel, hdfs, etc…

# Read a comma-separated values (csv) file into DataFrame.

economics = pd.read_csv(url_economics, index_col='date', parse_dates=True)

economics.head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

| 1967-09-01 |

516.3 |

199113 |

11.7 |

4.6 |

2958 |

#Export

# excel export depends on openpyxl

#> pip install openpyxl 2>&1 1>/dev/null

>

> �[1m[�[0m�[34;49mnotice�[0m�[1;39;49m]�[0m�[39;49m A new release of pip is available: �[0m�[31;49m23.3.1�[0m�[39;49m -> �[0m�[32;49m23.3.2�[0m

> �[1m[�[0m�[34;49mnotice�[0m�[1;39;49m]�[0m�[39;49m To update, run: �[0m�[32;49mpip install --upgrade pip�[0m

# Write DataFrame to a comma-separated values (csv) file.

economics.to_csv(path_or_buf="data.csv", index=False)

# and actual saving dataframe to excel

economics.to_excel("data.xlsx")

#> unlink data.xlsx

#> unlink data.csv

#Export to data structures

dfdict = economics.to_dict()

ic(len(dfdict))

ic(dfdict.keys())

> ic> len(dfdict): 5

> ic> dfdict.keys(): dict_keys(['pce', 'pop', 'psavert', 'uempmed', 'unemploy'])

result >>> dict_keys(['pce', 'pop', 'psavert', 'uempmed', 'unemploy'])

#Data: Indexing

#pd.Index

# manualy created index

indexes=pd.Index([0,1,2,3,4,5,6])

ic(type(indexes))

ic(indexes.size)

ic(indexes.shape)

ic(indexes.dtype)

> ic> type(indexes): <class 'pandas.core.indexes.numeric.Int64Index'>

> ic> indexes.size: 7

> ic> indexes.shape: (7,)

> ic> indexes.dtype: dtype('int64')

result >>> dtype('int64')

Create index and sort index on existing dataframe

economics.set_index('unemploy').sort_index().head(5)

|

pce |

pop |

psavert |

uempmed |

| unemploy |

|

|

|

|

| 2685 |

577.2 |

201621 |

10.9 |

4.4 |

| 2686 |

568.8 |

201095 |

10.4 |

4.6 |

| 2689 |

572.3 |

201290 |

10.6 |

4.8 |

| 2692 |

589.5 |

201881 |

9.4 |

4.9 |

| 2709 |

544.6 |

200208 |

12.2 |

4.6 |

and reset index

economics.set_index('unemploy').reset_index().head(2)

|

unemploy |

pce |

pop |

psavert |

uempmed |

| 0 |

2944 |

507.4 |

198712 |

12.5 |

4.5 |

| 1 |

2945 |

510.5 |

198911 |

12.5 |

4.7 |

#pd.DatetimeIndex

https://docs.scipy.org/doc/numpy/reference/arrays.datetime.html

# we can use numpy generated arrys for indexes or data

np.arange('1993-01-01', '1993-01-20', dtype="datetime64[W]")

result >>> array(['1992-12-31', '1993-01-07'], dtype='datetime64[W]')

# date generation

pd.date_range("2001-01-01", periods=3, freq="w")

result >>> DatetimeIndex(['2001-01-07', '2001-01-14', '2001-01-21'], dtype='datetime64[ns]', freq='W-SUN')

# autoguessing date format

pd.to_datetime(['1/2/2018', 'Jan 04, 2018'])

result >>> DatetimeIndex(['2018-01-02', '2018-01-04'], dtype='datetime64[ns]', freq=None)

# providing dateformat

pd.to_datetime(['2/1/2018', '6/1/2018'], format="%d/%m/%Y")

result >>> DatetimeIndex(['2018-01-02', '2018-01-06'], dtype='datetime64[ns]', freq=None)

# bussines days

pd.date_range("2018-01-02", periods=3, freq='B')

result >>> DatetimeIndex(['2018-01-02', '2018-01-03', '2018-01-04'], dtype='datetime64[ns]', freq='B')

Parsing dates

economics = pd.read_csv(url_economics, parse_dates=True)

economics.head(3)

|

date |

pce |

pop |

psavert |

uempmed |

unemploy |

| 0 |

1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1 |

1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

| 2 |

1967-09-01 |

516.3 |

199113 |

11.7 |

4.6 |

2958 |

pd.to_datetime(economics['date'], format='%Y-%m-%d').dt.strftime("%Y")[1:4]

result >>> 1 1967

result >>> 2 1967

result >>> 3 1967

result >>> Name: date, dtype: object

post load datetime transformation

economics = pd.read_csv(url_economics)

economics['date'] = pd.to_datetime(economics['date'])

economics.set_index('date',inplace=True)

economics.head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

| 1967-09-01 |

516.3 |

199113 |

11.7 |

4.6 |

2958 |

#Labels

tmp = pd.Series(['Oleg', 'Developer'], index=['person', 'who'])

# loc allow to request data by named index

# iloc allow to request data by numeric index

ic(tmp.loc['person'])

ic(tmp.iloc[1])

> ic> tmp.loc['person']: 'Oleg'

> ic> tmp.iloc[1]: 'Developer'

result >>> 'Developer'

tmp = pd.Series(range(26), index=[x for x in 'ABCDEFGHIJKLMNOPQRSTUVWXYZ'])

ic(tmp[3:9].values)

ic(tmp["D":"I"].values)

ic(tmp.iloc[3:9].values)

> ic> tmp[3:9].values: array([3, 4, 5, 6, 7, 8])

> ic> tmp["D":"I"].values: array([3, 4, 5, 6, 7, 8])

> ic> tmp.iloc[3:9].values: array([3, 4, 5, 6, 7, 8])

result >>> array([3, 4, 5, 6, 7, 8])

re-labeling / re-indexing

# reindexing

tmp.index = [x for x in 'GATTACAHIJKLMNOPQRSTUVWXYZ']

ic(tmp.loc['G'])

# Requesting non uniq values

try:

tmp.loc['G':'A']

except KeyError as e:

printError(e)

stderr> Error: "Cannot get right slice bound for non-unique label: 'A'"

#Index Based Access

economics = pd.read_csv(url_economics, index_col=["date"], parse_dates=True)

economics.head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

| 1967-09-01 |

516.3 |

199113 |

11.7 |

4.6 |

2958 |

# access top data using column name

economics["unemploy"].head(2)

result >>> date

result >>> 1967-07-01 2944

result >>> 1967-08-01 2945

result >>> Name: unemploy, dtype: int64

# or using column as property

economics.unemploy.head(2)

result >>> date

result >>> 1967-07-01 2944

result >>> 1967-08-01 2945

result >>> Name: unemploy, dtype: int64

economics.iloc[[0], :]

economics.iloc[[0,2,5,4], [0,1,2]]

|

pce |

pop |

psavert |

| date |

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

| 1967-09-01 |

516.3 |

199113 |

11.7 |

| 1967-12-01 |

525.8 |

199657 |

12.1 |

| 1967-11-01 |

518.1 |

199498 |

12.5 |

economics[['pce', 'pop']].head(2)

|

pce |

pop |

| date |

|

|

| 1967-07-01 |

507.4 |

198712 |

| 1967-08-01 |

510.5 |

198911 |

loc based indexing

# ranges and selections

economics.loc['1967-07-01':'1967-09-01', ['pop', 'pce']].head(2)

|

pop |

pce |

| date |

|

|

| 1967-07-01 |

198712 |

507.4 |

| 1967-08-01 |

198911 |

510.5 |

# ranges and ALL

economics.loc['1967-07-01':'1967-09-01', :].head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

# ranges and ranges

economics.loc['1967-07-01':'1967-09-01', 'pce':'psavert'].head(2)

|

pce |

pop |

psavert |

| date |

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

iloc based indexes

# ranges and ALL

economics.iloc[0:5,:].head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

# ranges and selection

economics.iloc[0:5,[0,3,4]].head(2)

|

pce |

uempmed |

unemploy |

| date |

|

|

|

| 1967-07-01 |

507.4 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

4.7 |

2945 |

# ranges and ranges

economics.iloc[0:5, 2:4].head(2)

|

psavert |

uempmed |

| date |

|

|

| 1967-07-01 |

12.5 |

4.5 |

| 1967-08-01 |

12.5 |

4.7 |

# combining different aproaches

pd.concat([

economics.iloc[0:1, 2:4],

economics.iloc[6:7, 2:4],

economics.loc['1978-07-01':'1978-09-01', ['psavert','uempmed']],

]).head(3)

|

psavert |

uempmed |

| date |

|

|

| 1967-07-01 |

12.5 |

4.5 |

| 1968-01-01 |

11.7 |

5.1 |

| 1978-07-01 |

10.3 |

5.8 |

# combining preselected columns with loc.

economics[['pce', 'unemploy']].loc['1967-07-01':'1969-07-01'].head(2)

|

pce |

unemploy |

| date |

|

|

| 1967-07-01 |

507.4 |

2944 |

| 1967-08-01 |

510.5 |

2945 |

# combining preselected columns with loc.

economics[['pce', 'unemploy']].iloc[10:14].head(2)

|

pce |

unemploy |

| date |

|

|

| 1968-05-01 |

550.4 |

2740 |

| 1968-06-01 |

556.8 |

2938 |

#Conditional Indexes

economics.loc[((economics.pce <= 630) & (economics.pce >= 600)), ['psavert', 'unemploy']].head(2)

|

psavert |

unemploy |

| date |

|

|

| 1969-05-01 |

10.0 |

2713 |

| 1969-06-01 |

10.9 |

2816 |

#Labeled Indexes (2)

size = 10

tmp = pd.DataFrame(rnd.randint(0, 10, size**2).reshape(size, -1),

index=[f"R{x:02d}" for x in range(size)],

columns = [f"C{x:02d}" for x in range(size)])

tmp

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

C07 |

C08 |

C09 |

| R00 |

7 |

2 |

5 |

4 |

1 |

7 |

5 |

1 |

4 |

0 |

| R01 |

9 |

5 |

8 |

0 |

9 |

2 |

6 |

3 |

8 |

2 |

| R02 |

4 |

2 |

6 |

4 |

8 |

6 |

1 |

3 |

8 |

1 |

| R03 |

9 |

8 |

9 |

4 |

1 |

3 |

6 |

7 |

2 |

0 |

| R04 |

3 |

1 |

7 |

3 |

1 |

5 |

5 |

9 |

3 |

5 |

| R05 |

1 |

9 |

1 |

9 |

3 |

7 |

6 |

8 |

7 |

4 |

| R06 |

1 |

4 |

7 |

9 |

8 |

8 |

0 |

8 |

6 |

8 |

| R07 |

7 |

0 |

7 |

7 |

2 |

0 |

7 |

2 |

2 |

0 |

| R08 |

4 |

9 |

6 |

9 |

8 |

6 |

8 |

7 |

1 |

0 |

| R09 |

6 |

6 |

7 |

4 |

2 |

7 |

5 |

2 |

0 |

2 |

# rows not found.

tmp['C05':'C09']

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

C07 |

C08 |

C09 |

# but as column its ok!

tmp['C05']

result >>> R00 7

result >>> R01 2

result >>> R02 6

result >>> R03 3

result >>> R04 5

result >>> R05 7

result >>> R06 8

result >>> R07 0

result >>> R08 6

result >>> R09 7

result >>> Name: C05, dtype: int64

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

C07 |

C08 |

C09 |

| R05 |

1 |

9 |

1 |

9 |

3 |

7 |

6 |

8 |

7 |

4 |

| R06 |

1 |

4 |

7 |

9 |

8 |

8 |

0 |

8 |

6 |

8 |

#MultiIndex

pdlen = 20

tmp = pd.DataFrame(

{

'city' : [x for x in ['Paris', 'London', 'Berlin', 'Manchester', 'Kyiv']*10][:pdlen],

'category' : rnd.randint(0, 7, pdlen),

'price' : rnd.randint(10, 300, pdlen),

'rating' : rnd.randint(0, 5, pdlen),

}

)

tmp['country'] = tmp['city'].map({

'Paris':'FR',

'London':'UK',

'Berlin':'DE',

'Manchester':'US',

'Kyiv':'UA',

})

tmp.head(5)

|

city |

category |

price |

rating |

country |

| 0 |

Paris |

4 |

72 |

4 |

FR |

| 1 |

London |

6 |

240 |

0 |

UK |

| 2 |

Berlin |

5 |

250 |

4 |

DE |

| 3 |

Manchester |

2 |

61 |

3 |

US |

| 4 |

Kyiv |

0 |

105 |

3 |

UA |

tmp = tmp.groupby(['country', 'city', 'category']).mean()

tmp

|

|

|

price |

rating |

| country |

city |

category |

|

|

| DE |

Berlin |

0 |

22.0 |

0.0 |

| 3 |

293.0 |

3.0 |

| 5 |

250.0 |

4.0 |

| 6 |

246.0 |

3.0 |

| FR |

Paris |

1 |

252.0 |

2.0 |

| 4 |

151.5 |

3.5 |

| 6 |

38.0 |

3.0 |

| UA |

Kyiv |

0 |

105.0 |

3.0 |

| 2 |

179.0 |

0.0 |

| 5 |

180.0 |

1.0 |

| 6 |

196.0 |

0.0 |

| UK |

London |

1 |

167.5 |

1.5 |

| 2 |

45.0 |

0.0 |

| 6 |

240.0 |

0.0 |

| US |

Manchester |

2 |

61.0 |

3.0 |

| 4 |

75.0 |

4.0 |

| 6 |

160.5 |

1.0 |

# show all indexes and levels

ic(tmp.index)

ic(tmp.index.levels)

print("-"*70)

ic(tmp.index.names)

ic(tmp.index.values)

print("-"*70)

ic(tmp.index.get_level_values(2))

print("-"*70)

ic(tmp.loc["UA"])

print("-"*70)

ic(tmp.loc["UA", "Kyiv"].max())

ic(tmp.loc["UA", "Kyiv", 0:4])

> ic> tmp.index: MultiIndex([('DE', 'Berlin', 0), ('DE', 'Berlin', 3), ('DE', 'Berlin', 5), ('DE', 'Berlin', 6), ('FR', 'Paris', 1), ('FR', 'Paris', 4), ('FR', 'Paris', 6), ('UA', 'Kyiv', 0), ('UA', 'Kyiv', 2), ('UA', 'Kyiv', 5), ('UA', 'Kyiv', 6), ('UK', 'London', 1), ('UK', 'London', 2), ('UK', 'London', 6), ('US', 'Manchester', 2), ('US', 'Manchester', 4), ('US', 'Manchester', 6)], names=['country', 'city', 'category'])

> ic> tmp.index.levels: FrozenList([['DE', 'FR', 'UA', 'UK', 'US'], ['Berlin', 'Kyiv', 'London', 'Manchester', 'Paris'], [0, 1, 2, 3, 4, 5, 6]])

> ----------------------------------------------------------------------

> ic> tmp.index.names: FrozenList(['country', 'city', 'category'])

> ic> tmp.index.values: array([('DE', 'Berlin', 0), ('DE', 'Berlin', 3), ('DE', 'Berlin', 5), ('DE', 'Berlin', 6), ('FR', 'Paris', 1), ('FR', 'Paris', 4), ('FR', 'Paris', 6), ('UA', 'Kyiv', 0), ('UA', 'Kyiv', 2), ('UA', 'Kyiv', 5), ('UA', 'Kyiv', 6), ('UK', 'London', 1), ('UK', 'London', 2), ('UK', 'London', 6), ('US', 'Manchester', 2), ('US', 'Manchester', 4), ('US', 'Manchester', 6)], dtype=object)

> ----------------------------------------------------------------------

> ic> tmp.index.get_level_values(2): Int64Index([0, 3, 5, 6, 1, 4, 6, 0, 2, 5, 6, 1, 2, 6, 2, 4, 6], dtype='int64', name='category')

> ----------------------------------------------------------------------

> ic> tmp.loc["UA"]: price rating

> city category

> Kyiv 0 105.0 3.0

> 2 179.0 0.0

> 5 180.0 1.0

> 6 196.0 0.0

> ----------------------------------------------------------------------

> ic> tmp.loc["UA", "Kyiv"].max(): price 196.0

> rating 3.0

> dtype: float64

> ic> tmp.loc["UA", "Kyiv", 0:4]: price rating

> country city category

> UA Kyiv 0 105.0 3.0

> 2 179.0 0.0

|

|

|

price |

rating |

| country |

city |

category |

|

|

| UA |

Kyiv |

0 |

105.0 |

3.0 |

| 2 |

179.0 |

0.0 |

# without inplace=True it will return new dataframe

tmp.rename(index={'UA':'ЮА'}, columns={'price':'Precio'}, inplace=True)

tmp

|

|

|

Precio |

rating |

| country |

city |

category |

|

|

| DE |

Berlin |

0 |

22.0 |

0.0 |

| 3 |

293.0 |

3.0 |

| 5 |

250.0 |

4.0 |

| 6 |

246.0 |

3.0 |

| FR |

Paris |

1 |

252.0 |

2.0 |

| 4 |

151.5 |

3.5 |

| 6 |

38.0 |

3.0 |

| ЮА |

Kyiv |

0 |

105.0 |

3.0 |

| 2 |

179.0 |

0.0 |

| 5 |

180.0 |

1.0 |

| 6 |

196.0 |

0.0 |

| UK |

London |

1 |

167.5 |

1.5 |

| 2 |

45.0 |

0.0 |

| 6 |

240.0 |

0.0 |

| US |

Manchester |

2 |

61.0 |

3.0 |

| 4 |

75.0 |

4.0 |

| 6 |

160.5 |

1.0 |

#pd.Index as Sets

# intersection

ic(pd.Index([1,2,3,4]) & pd.Index([3,4,5,6]))

# union

ic(pd.Index([1,2,3,4]) | pd.Index([3,4,5,6]))

# symetric difference

ic(pd.Index([1,2,3,4]) ^ pd.Index([3,4,5,6]))

stderr> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/1864070959.py:2: FutureWarning: Index.__and__ operating as a set operation is deprecated, in the future this will be a logical operation matching Series.__and__. Use index.intersection(other) instead.

stderr> ic(pd.Index([1,2,3,4]) & pd.Index([3,4,5,6]))

stderr> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/1864070959.py:5: FutureWarning: Index.__or__ operating as a set operation is deprecated, in the future this will be a logical operation matching Series.__or__. Use index.union(other) instead.

stderr> ic(pd.Index([1,2,3,4]) | pd.Index([3,4,5,6]))

stderr> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/1864070959.py:8: FutureWarning: Index.__xor__ operating as a set operation is deprecated, in the future this will be a logical operation matching Series.__xor__. Use index.symmetric_difference(other) instead.

stderr> ic(pd.Index([1,2,3,4]) ^ pd.Index([3,4,5,6]))

result >>> Int64Index([1, 2, 5, 6], dtype='int64')

#Index Aligment

# source data area and population

data_area = { 'Alaska': 1723337, 'Texas': 695662, 'California': 423967}

data_ppls = { 'California': 38332521, 'Texas': 26448193, 'New York': 19651127}

area = pd.Series(data_area, name='area')

ppls = pd.Series(data_ppls, name='ppls')

# Index aligment

ic(ppls/area)

> ic> ppls/area: Alaska NaN

> California 90.413926

> New York NaN

> Texas 38.018740

> dtype: float64

result >>> Alaska NaN

result >>> California 90.413926

result >>> New York NaN

result >>> Texas 38.018740

result >>> dtype: float64

One more example

A = pd.Series([2, 4, 6], index=[0, 1, 2])

B = pd.Series([1, 3, 5], index=[1, 2, 3])

ic(A+B)

> ic> A+B: 0 NaN

> 1 5.0

> 2 9.0

> 3 NaN

> dtype: float64

result >>> 0 NaN

result >>> 1 5.0

result >>> 2 9.0

result >>> 3 NaN

result >>> dtype: float64

using functions methods (.add() instead + ) we can fill nan values

# using function we can fill nan values

ic(A.add(B, fill_value=100))

> ic> A.add(B, fill_value=100): 0 102.0

> 1 5.0

> 2 9.0

> 3 105.0

> dtype: float64

result >>> 0 102.0

result >>> 1 5.0

result >>> 2 9.0

result >>> 3 105.0

result >>> dtype: float64

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

ic(economics.unemploy.idxmin())

ic(economics.unemploy.min())

ic(np.argmin(economics.unemploy))

print("-"*60)

ic(economics.unemploy.idxmax())

ic(economics.unemploy.max())

ic(np.argmax(economics.unemploy))

> ic> economics.unemploy.idxmin(): Timestamp('1968-12-01 00:00:00')

> ic> economics.unemploy.min(): 2685

> ic> np.argmin(economics.unemploy): 17

> ------------------------------------------------------------

> ic> economics.unemploy.idxmax(): Timestamp('2009-10-01 00:00:00')

> ic> economics.unemploy.max(): 15352

> ic> np.argmax(economics.unemploy): 507

result >>> 507

#Data: Handling Data

#Handling Missing Data

titanic = pd.read_csv(url_titanic, keep_default_na=False)

titanic['age'][4:7].head()

result >>> 4 35.0

result >>> 5

result >>> 6 54.0

result >>> Name: age, dtype: object

# Additional strings to recognize as NA/NaN.

# If dict passed, specific per-column NA values.

# By default the following values are interpreted as

# NaN: ‘’, ‘#N/A’, ‘#N/A N/A’, ‘#NA’, ‘-1.#IND’, ‘-1.#QNAN’, ‘-NaN’,

# ‘-nan’, ‘1.#IND’, ‘1.#QNAN’, ‘N/A’, ‘NA’, ‘NULL’, ‘NaN’, ‘n/a’, ‘nan’, ‘null’.

titanic = pd.read_csv(url_titanic, na_values=[35.0])

titanic['age'][4:7].head()

result >>> 4 NaN

result >>> 5 NaN

result >>> 6 54.0

result >>> Name: age, dtype: float64

titanic = pd.read_csv(url_titanic, keep_default_na=True)

titanic['age'][4:7].head()

result >>> 4 35.0

result >>> 5 NaN

result >>> 6 54.0

result >>> Name: age, dtype: float64

ic(titanic['age'].hasnans)

ic(titanic['age'].isnull().sum())

ic(titanic['age'].dropna().hasnans)

ic(titanic['age'].dropna().isnull().sum())

ic(titanic['age'].notnull().sum())

ic(np.count_nonzero(titanic['age'].isnull()))

> ic> titanic['age'].hasnans: True

> ic> titanic['age'].isnull().sum(): 177

> ic> titanic['age'].dropna().hasnans: False

> ic> titanic['age'].dropna().isnull().sum(): 0

> ic> titanic['age'].notnull().sum(): 714

> ic> np.count_nonzero(titanic['age'].isnull()): 177

result >>> 177

titanic.age.value_counts(dropna=True).plot.pie()

getting rid of nans

ages = pd.DataFrame()

ages['fillna(0)'] = titanic['age'].fillna(0)

ages['fillna - ffill'] = titanic['age'].fillna(method='ffill')

ages['fillna - bfill'] = titanic['age'].fillna(method='bfill')

ages['dropna'] = titanic['age'].dropna(inplace=False )

ages['interpolate'] = titanic['age'].interpolate()

ages['min'] = titanic['age'].fillna(titanic['age'].min())

ages['mean'] = titanic['age'].fillna(titanic['age'].mean())

ages[4:7]

|

fillna(0) |

fillna - ffill |

fillna - bfill |

dropna |

interpolate |

min |

mean |

| 4 |

35.0 |

35.0 |

35.0 |

35.0 |

35.0 |

35.00 |

35.000000 |

| 5 |

0.0 |

35.0 |

54.0 |

NaN |

44.5 |

0.42 |

29.699118 |

| 6 |

54.0 |

54.0 |

54.0 |

54.0 |

54.0 |

54.00 |

54.000000 |

#Melting/Mergin/Concating Data

titanic = pd.read_csv(url_titanic, keep_default_na=True)

titanic.head(3)

|

survived |

pclass |

sex |

age |

sibsp |

parch |

fare |

embarked |

class |

who |

adult_male |

deck |

embark_town |

alive |

alone |

| 0 |

0 |

3 |

male |

22.0 |

1 |

0 |

7.2500 |

S |

Third |

man |

True |

NaN |

Southampton |

no |

False |

| 1 |

1 |

1 |

female |

38.0 |

1 |

0 |

71.2833 |

C |

First |

woman |

False |

C |

Cherbourg |

yes |

False |

| 2 |

1 |

3 |

female |

26.0 |

0 |

0 |

7.9250 |

S |

Third |

woman |

False |

NaN |

Southampton |

yes |

True |

Renaming columns and indexes

titanic.rename(columns={'sex':'gender'}, inplace=True)

titanic.head(3)

|

survived |

pclass |

gender |

age |

sibsp |

parch |

fare |

embarked |

class |

who |

adult_male |

deck |

embark_town |

alive |

alone |

| 0 |

0 |

3 |

male |

22.0 |

1 |

0 |

7.2500 |

S |

Third |

man |

True |

NaN |

Southampton |

no |

False |

| 1 |

1 |

1 |

female |

38.0 |

1 |

0 |

71.2833 |

C |

First |

woman |

False |

C |

Cherbourg |

yes |

False |

| 2 |

1 |

3 |

female |

26.0 |

0 |

0 |

7.9250 |

S |

Third |

woman |

False |

NaN |

Southampton |

yes |

True |

droping columns

titanic.drop('embarked', axis=1, errors="ignore", inplace=True)

titanic.drop('who', axis=1, errors="ignore", inplace=True)

titanic.drop(['adult_male', 'alone'], axis=1, errors="ignore", inplace=True)

titanic.drop(['parch', 'deck'], axis=1, errors="ignore", inplace=True)

titanic.head(3)

|

survived |

pclass |

gender |

age |

sibsp |

fare |

class |

embark_town |

alive |

| 0 |

0 |

3 |

male |

22.0 |

1 |

7.2500 |

Third |

Southampton |

no |

| 1 |

1 |

1 |

female |

38.0 |

1 |

71.2833 |

First |

Cherbourg |

yes |

| 2 |

1 |

3 |

female |

26.0 |

0 |

7.9250 |

Third |

Southampton |

yes |

# fares

titanic = titanic.groupby(['class', 'embark_town', 'gender'])['age'].mean().reset_index()

titanic

|

class |

embark_town |

gender |

age |

| 0 |

First |

Cherbourg |

female |

36.052632 |

| 1 |

First |

Cherbourg |

male |

40.111111 |

| 2 |

First |

Queenstown |

female |

33.000000 |

| 3 |

First |

Queenstown |

male |

44.000000 |

| 4 |

First |

Southampton |

female |

32.704545 |

| 5 |

First |

Southampton |

male |

41.897188 |

| 6 |

Second |

Cherbourg |

female |

19.142857 |

| 7 |

Second |

Cherbourg |

male |

25.937500 |

| 8 |

Second |

Queenstown |

female |

30.000000 |

| 9 |

Second |

Queenstown |

male |

57.000000 |

| 10 |

Second |

Southampton |

female |

29.719697 |

| 11 |

Second |

Southampton |

male |

30.875889 |

| 12 |

Third |

Cherbourg |

female |

14.062500 |

| 13 |

Third |

Cherbourg |

male |

25.016800 |

| 14 |

Third |

Queenstown |

female |

22.850000 |

| 15 |

Third |

Queenstown |

male |

28.142857 |

| 16 |

Third |

Southampton |

female |

23.223684 |

| 17 |

Third |

Southampton |

male |

26.574766 |

pivoting data

titanic.pivot_table(index=['class','gender'],columns='embark_town',values='age').reset_index().head(3)

| embark_town |

class |

gender |

Cherbourg |

Queenstown |

Southampton |

| 0 |

First |

female |

36.052632 |

33.0 |

32.704545 |

| 1 |

First |

male |

40.111111 |

44.0 |

41.897188 |

| 2 |

Second |

female |

19.142857 |

30.0 |

29.719697 |

melting data

pd.melt(titanic, id_vars=['class', 'gender']).head(3)

|

class |

gender |

variable |

value |

| 0 |

First |

female |

embark_town |

Cherbourg |

| 1 |

First |

male |

embark_town |

Cherbourg |

| 2 |

First |

female |

embark_town |

Queenstown |

# todo - cover

# unstack()

# stack()

#Common Math operations over the DataFrames/Series

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.info()

> <class 'pandas.core.frame.DataFrame'>

> DatetimeIndex: 574 entries, 1967-07-01 to 2015-04-01

> Data columns (total 5 columns):

> # Column Non-Null Count Dtype

> --- ------ -------------- -----

> 0 pce 574 non-null float64

> 1 pop 574 non-null int64

> 2 psavert 574 non-null float64

> 3 uempmed 574 non-null float64

> 4 unemploy 574 non-null int64

> dtypes: float64(3), int64(2)

> memory usage: 26.9 KB

|

pce |

pop |

psavert |

uempmed |

unemploy |

| count |

574.000000 |

574.000000 |

574.000000 |

574.000000 |

574.000000 |

| mean |

4843.510453 |

257189.381533 |

7.936585 |

8.610105 |

7771.557491 |

| std |

3579.287206 |

36730.801593 |

3.124394 |

4.108112 |

2641.960571 |

| min |

507.400000 |

198712.000000 |

1.900000 |

4.000000 |

2685.000000 |

| 25% |

1582.225000 |

224896.000000 |

5.500000 |

6.000000 |

6284.000000 |

| 50% |

3953.550000 |

253060.000000 |

7.700000 |

7.500000 |

7494.000000 |

| 75% |

7667.325000 |

290290.750000 |

10.500000 |

9.100000 |

8691.000000 |

| max |

12161.500000 |

320887.000000 |

17.000000 |

25.200000 |

15352.000000 |

economics.pce.mean()

result >>> 4843.510452961673

economics.pce = economics.pce * 2

economics.head()

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

1014.8 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

1021.0 |

198911 |

12.5 |

4.7 |

2945 |

| 1967-09-01 |

1032.6 |

199113 |

11.7 |

4.6 |

2958 |

| 1967-10-01 |

1025.8 |

199311 |

12.5 |

4.9 |

3143 |

| 1967-11-01 |

1036.2 |

199498 |

12.5 |

4.7 |

3066 |

cs = economics.pce.cumsum()

ic(cs.head(1))

ic(cs.tail(1))

> ic> cs.head(1): date

> 1967-07-01 1014.8

> Name: pce, dtype: float64

> ic> cs.tail(1): date

> 2015-04-01 5560350.0

> Name: pce, dtype: float64

result >>> date

result >>> 2015-04-01 5560350.0

result >>> Name: pce, dtype: float64

#Math operations over the DataFrames/Series

Using aplly over column data

titanic = pd.read_csv(url_titanic, keep_default_na=True)

titanic.head(3)

|

survived |

pclass |

sex |

age |

sibsp |

parch |

fare |

embarked |

class |

who |

adult_male |

deck |

embark_town |

alive |

alone |

| 0 |

0 |

3 |

male |

22.0 |

1 |

0 |

7.2500 |

S |

Third |

man |

True |

NaN |

Southampton |

no |

False |

| 1 |

1 |

1 |

female |

38.0 |

1 |

0 |

71.2833 |

C |

First |

woman |

False |

C |

Cherbourg |

yes |

False |

| 2 |

1 |

3 |

female |

26.0 |

0 |

0 |

7.9250 |

S |

Third |

woman |

False |

NaN |

Southampton |

yes |

True |

def my_mean(vector):

return vector * 5

titanic.rename(columns={'fare':'1912_£'}, inplace=True)

titanic['1912_$'] = titanic['1912_£'].apply(my_mean)

titanic.loc[:, ['class', '1912_£', '1912_$']].head(5)

|

class |

1912_£ |

1912_$ |

| 0 |

Third |

7.2500 |

36.2500 |

| 1 |

First |

71.2833 |

356.4165 |

| 2 |

Third |

7.9250 |

39.6250 |

| 3 |

First |

53.1000 |

265.5000 |

| 4 |

Third |

8.0500 |

40.2500 |

#Grouped Calculations

df = pd.read_csv(url_economics, parse_dates=['date'])

ic(df['date'].dtypes)

> ic> df['date'].dtypes: dtype('<M8[ns]')

result >>> dtype('<M8[ns]')

df.groupby('date')['pce', 'unemploy'].mean().head(10)

> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/3677347823.py:1: FutureWarning: Indexing with multiple keys (implicitly converted to a tuple of keys) will be deprecated, use a list instead.

> df.groupby('date')['pce', 'unemploy'].mean().head(10)

|

pce |

unemploy |

| date |

|

|

| 1967-07-01 |

507.4 |

2944.0 |

| 1967-08-01 |

510.5 |

2945.0 |

| 1967-09-01 |

516.3 |

2958.0 |

| 1967-10-01 |

512.9 |

3143.0 |

| 1967-11-01 |

518.1 |

3066.0 |

| 1967-12-01 |

525.8 |

3018.0 |

| 1968-01-01 |

531.5 |

2878.0 |

| 1968-02-01 |

534.2 |

3001.0 |

| 1968-03-01 |

544.9 |

2877.0 |

| 1968-04-01 |

544.6 |

2709.0 |

df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].mean().reset_index().head(3)

> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/1916814624.py:1: FutureWarning: Indexing with multiple keys (implicitly converted to a tuple of keys) will be deprecated, use a list instead.

> df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].mean().reset_index().head(3)

|

date |

unemploy |

uempmed |

| 0 |

1967 |

3012.333333 |

4.700000 |

| 1 |

1968 |

2797.416667 |

4.500000 |

| 2 |

1969 |

2830.166667 |

4.441667 |

df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].first().reset_index().head(3)

> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/2747298252.py:1: FutureWarning: Indexing with multiple keys (implicitly converted to a tuple of keys) will be deprecated, use a list instead.

> df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].first().reset_index().head(3)

|

date |

unemploy |

uempmed |

| 0 |

1967 |

2944 |

4.5 |

| 1 |

1968 |

2878 |

5.1 |

| 2 |

1969 |

2718 |

4.4 |

df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].last().reset_index().head(3)

> /var/folders/7j/8x_gv0vs7f33q1cxc5cyhl3r0000gn/T/ipykernel_29394/3124120651.py:1: FutureWarning: Indexing with multiple keys (implicitly converted to a tuple of keys) will be deprecated, use a list instead.

> df.groupby(by=df['date'].dt.strftime('%Y'))['unemploy', 'uempmed'].last().reset_index().head(3)

|

date |

unemploy |

uempmed |

| 0 |

1967 |

3018 |

4.8 |

| 1 |

1968 |

2685 |

4.4 |

| 2 |

1969 |

2884 |

4.6 |

#Joins

size = 6

df_square = pd.DataFrame(rnd.randint(0, 10, size**2).reshape(size, -1),

index=[f"R{x:02d}" for x in range(size)],

columns = [f"C{x:02d}" for x in range(size)])

df_square

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

| R00 |

2 |

6 |

5 |

7 |

8 |

4 |

| R01 |

0 |

2 |

9 |

7 |

5 |

7 |

| R02 |

8 |

3 |

0 |

0 |

9 |

3 |

| R03 |

6 |

1 |

2 |

0 |

4 |

0 |

| R04 |

7 |

0 |

0 |

1 |

1 |

5 |

| R05 |

6 |

4 |

0 |

0 |

2 |

1 |

df_line = pd.Series(rnd.randint(0, 10, size), index=[f"R{x+3:02d}" for x in range(size)])

df_line.name="C06"

df_line

result >>> R03 4

result >>> R04 9

result >>> R05 5

result >>> R06 6

result >>> R07 3

result >>> R08 6

result >>> Name: C06, dtype: int64

df_square['C06'] = df_line

df_square

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

| R00 |

2 |

6 |

5 |

7 |

8 |

4 |

NaN |

| R01 |

0 |

2 |

9 |

7 |

5 |

7 |

NaN |

| R02 |

8 |

3 |

0 |

0 |

9 |

3 |

NaN |

| R03 |

6 |

1 |

2 |

0 |

4 |

0 |

4.0 |

| R04 |

7 |

0 |

0 |

1 |

1 |

5 |

9.0 |

| R05 |

6 |

4 |

0 |

0 |

2 |

1 |

5.0 |

clean up data

df_square.drop('C06', axis=1, errors="ignore", inplace=True)

df_square.join(pd.DataFrame(df_line), how="inner")

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

| R03 |

6 |

1 |

2 |

0 |

4 |

0 |

4 |

| R04 |

7 |

0 |

0 |

1 |

1 |

5 |

9 |

| R05 |

6 |

4 |

0 |

0 |

2 |

1 |

5 |

df_square.join(pd.DataFrame(df_line), how="outer")

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

| R00 |

2.0 |

6.0 |

5.0 |

7.0 |

8.0 |

4.0 |

NaN |

| R01 |

0.0 |

2.0 |

9.0 |

7.0 |

5.0 |

7.0 |

NaN |

| R02 |

8.0 |

3.0 |

0.0 |

0.0 |

9.0 |

3.0 |

NaN |

| R03 |

6.0 |

1.0 |

2.0 |

0.0 |

4.0 |

0.0 |

4.0 |

| R04 |

7.0 |

0.0 |

0.0 |

1.0 |

1.0 |

5.0 |

9.0 |

| R05 |

6.0 |

4.0 |

0.0 |

0.0 |

2.0 |

1.0 |

5.0 |

| R06 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

6.0 |

| R07 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

3.0 |

| R08 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

6.0 |

df_square.join(pd.DataFrame(df_line), how="left")

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

| R00 |

2 |

6 |

5 |

7 |

8 |

4 |

NaN |

| R01 |

0 |

2 |

9 |

7 |

5 |

7 |

NaN |

| R02 |

8 |

3 |

0 |

0 |

9 |

3 |

NaN |

| R03 |

6 |

1 |

2 |

0 |

4 |

0 |

4.0 |

| R04 |

7 |

0 |

0 |

1 |

1 |

5 |

9.0 |

| R05 |

6 |

4 |

0 |

0 |

2 |

1 |

5.0 |

df_square.join(pd.DataFrame(df_line), how="right")

|

C00 |

C01 |

C02 |

C03 |

C04 |

C05 |

C06 |

| R03 |

6.0 |

1.0 |

2.0 |

0.0 |

4.0 |

0.0 |

4 |

| R04 |

7.0 |

0.0 |

0.0 |

1.0 |

1.0 |

5.0 |

9 |

| R05 |

6.0 |

4.0 |

0.0 |

0.0 |

2.0 |

1.0 |

5 |

| R06 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

6 |

| R07 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

3 |

| R08 |

NaN |

NaN |

NaN |

NaN |

NaN |

NaN |

6 |

#Sorting values and indexes

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.sort_values(by='unemploy', ascending=False).head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 2009-10-01 |

9924.6 |

308189 |

5.4 |

18.9 |

15352 |

| 2010-04-01 |

10106.9 |

309191 |

5.6 |

22.1 |

15325 |

| 2009-11-01 |

9946.1 |

308418 |

5.7 |

19.8 |

15219 |

economics.sort_index(ascending=False).head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 2015-04-01 |

12158.9 |

320887 |

5.6 |

11.7 |

8549 |

| 2015-03-01 |

12161.5 |

320707 |

5.2 |

12.2 |

8575 |

| 2015-02-01 |

12095.9 |

320534 |

5.7 |

13.1 |

8705 |

#Time Series Analisis

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

economics.index

result >>> DatetimeIndex(['1967-07-01', '1967-08-01', '1967-09-01', '1967-10-01',

result >>> '1967-11-01', '1967-12-01', '1968-01-01', '1968-02-01',

result >>> '1968-03-01', '1968-04-01',

result >>> ...

result >>> '2014-07-01', '2014-08-01', '2014-09-01', '2014-10-01',

result >>> '2014-11-01', '2014-12-01', '2015-01-01', '2015-02-01',

result >>> '2015-03-01', '2015-04-01'],

result >>> dtype='datetime64[ns]', name='date', length=574, freq=None)

TIME SERIES OFFSET ALIASES

| ALIAS |

DESCRIPTION |

| B |

business day frequency |

| C |

custom business day frequency (experimental) |

| D |

calendar day frequency |

| W |

weekly frequency |

| M |

month end frequency |

| SM |

semi-month end frequency (15th and end of month) |

| BM |

business month end frequency |

| CBM |

custom business month end frequency |

| MS |

month start frequency |

| SMS |

semi-month start frequency (1st and 15th) |

| BMS |

business month start frequency |

| CBMS |

custom business month start frequency |

| Q |

quarter end frequency |

| BQ |

business quarter endfrequency |

| QS |

quarter start frequency |

| BQS |

business quarter start frequency |

| A |

year end frequency |

| BA |

business year end frequency |

| AS |

year start frequency |

| BAS |

business year start frequency |

| BH |

business hour frequency |

| H |

hourly frequency |

| T, min |

minutely frequency |

| S |

secondly frequency |

| L, ms |

milliseconds |

| U, us |

microseconds |

| N |

nanoseconds |

#Time Resampling

# yearly

economics.resample(rule='A').mean().head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-12-31 |

515.166667 |

199200.333333 |

12.300000 |

4.700000 |

3012.333333 |

| 1968-12-31 |

557.458333 |

200663.750000 |

11.216667 |

4.500000 |

2797.416667 |

| 1969-12-31 |

604.483333 |

202648.666667 |

10.741667 |

4.441667 |

2830.166667 |

economics.resample(rule='A').first().head(3)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-12-31 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1968-12-31 |

531.5 |

199808 |

11.7 |

5.1 |

2878 |

| 1969-12-31 |

584.2 |

201760 |

10.0 |

4.4 |

2718 |

# custom resampling function

def total(entry):

if len(entry):

return entry.sum()

economics.unemploy.resample(rule='A').apply(total).head(2)

result >>> date

result >>> 1967-12-31 18074

result >>> 1968-12-31 33569

result >>> Freq: A-DEC, Name: unemploy, dtype: int64

#Time/Data Shifting

http://pandas.pydata.org/pandas-docs/stable/generated/pandas.DataFrame.shift.html

economics.unemploy.shift(1).head(2)

result >>> date

result >>> 1967-07-01 NaN

result >>> 1967-08-01 2944.0

result >>> Name: unemploy, dtype: float64

# Shift everything forward one month

economics.unemploy.shift(periods=2, freq='M').head()

result >>> date

result >>> 1967-08-31 2944

result >>> 1967-09-30 2945

result >>> 1967-10-31 2958

result >>> 1967-11-30 3143

result >>> 1967-12-31 3066

result >>> Name: unemploy, dtype: int64

#Rolling and Expanding

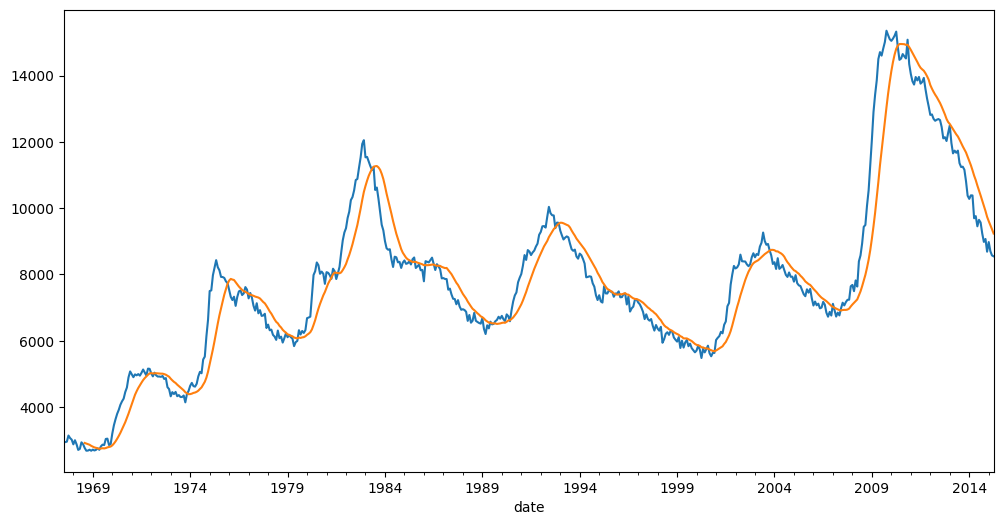

A common process with time series is to create data based off of a rolling mean. The idea is to divide the data into “windows” of time, and then calculate an aggregate function for each window. In this way we obtain a simple moving average.

economics.unemploy.plot(figsize=(12,6)).autoscale(axis='x',tight=True)

economics.unemploy.rolling(window=14).mean().plot()

# economics.unemploy.rolling(window=30).max().plot()

# economics.unemploy.rolling(window=30).min().plot()

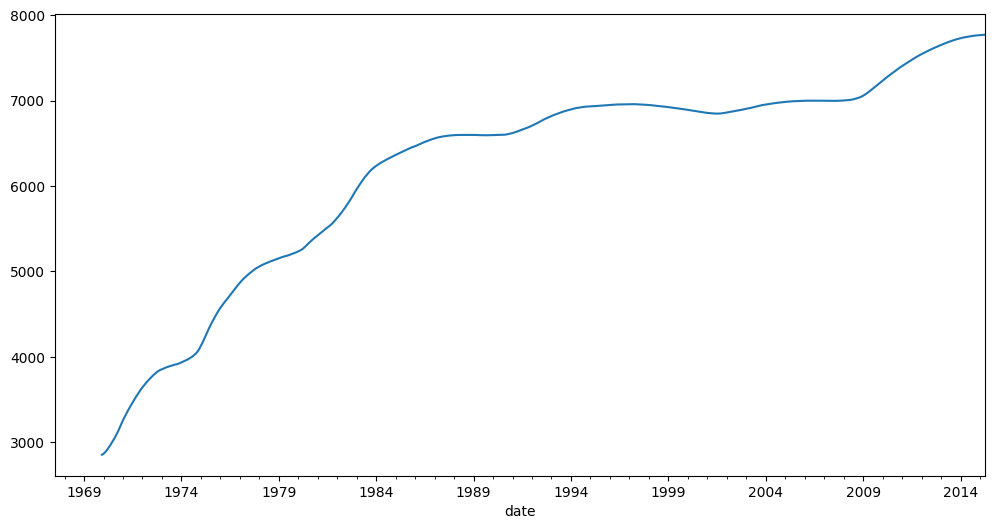

Instead of calculating values for a rolling window of dates, what if you wanted to take into account everything from the start of the time series up to each point in time? For example, instead of considering the average over the last 7 days, we would consider all prior data in our expanding set of averages.

economics.unemploy.expanding(min_periods=30).mean().plot(figsize=(12,6))

#Visualization

import matplotlib.pyplot as plt

%matplotlib inline

economics = pd.read_csv(url_economics, index_col='date',parse_dates=True)

economics.head(2)

|

pce |

pop |

psavert |

uempmed |

unemploy |

| date |

|

|

|

|

|

| 1967-07-01 |

507.4 |

198712 |

12.5 |

4.5 |

2944 |

| 1967-08-01 |

510.5 |

198911 |

12.5 |

4.7 |

2945 |

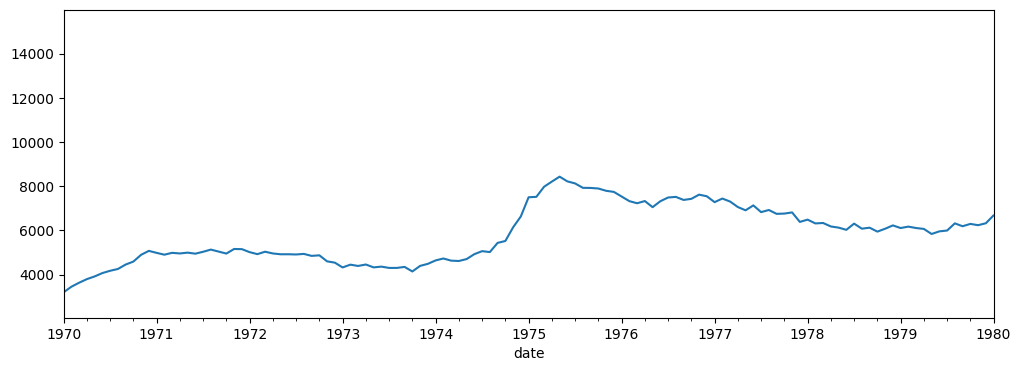

# ploting all data for a range of x values (date index)

_ = economics.unemploy.plot(

figsize=(12,4),

xlim=['1970', '1980'],

)

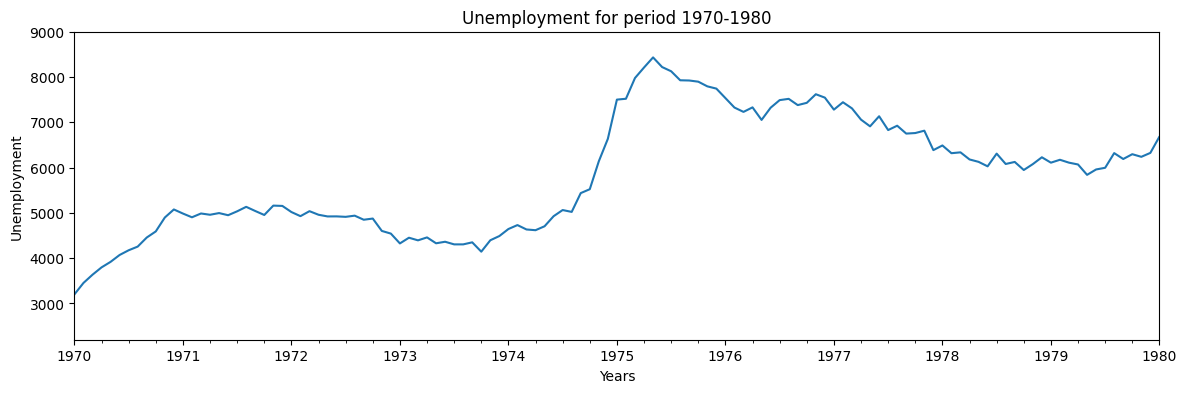

# or we can specify what column we want to plot

ax = economics['unemploy'].plot(

figsize=(14,4),

xlim=['1970', '1980'],

ylim=[2200, 9000],

title="Unemployment for period 1970-1980"

)

_ = ax.set(ylabel="Unemployment", xlabel="Years")

# this will make data to fit, no matter what we set in x

# ax.autoscale(axis='x',tight=True)

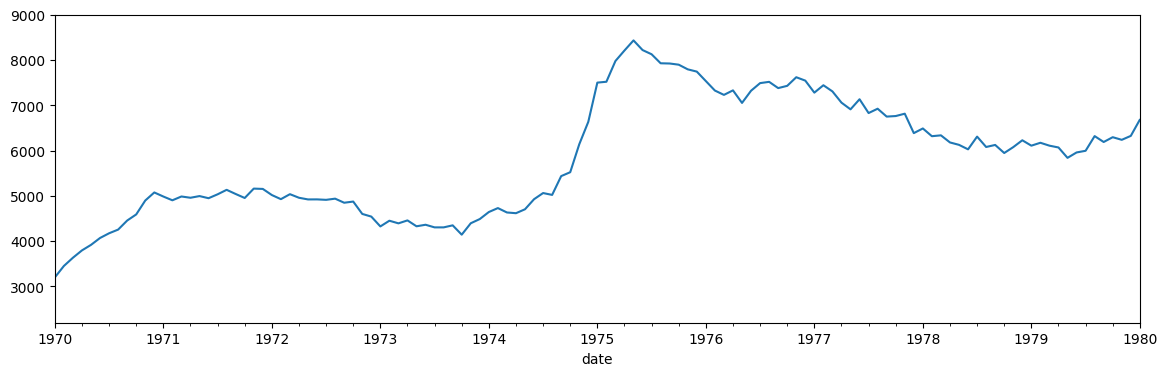

# x as slicing

economics['unemploy']['1970':'1979'].plot(figsize=(14,4), ls='--',c='r').autoscale(axis='x',tight=True)

# or providing argument

_ = economics['unemploy'].plot(figsize=(14,4), xlim=['1970','1980'], ylim=[2200, 9000])

#X-Ticks

https://matplotlib.org/api/dates_api.html

Formatting follows the Python datetime strftime codes.

The following examples are based on datetime.datetime(2001, 2, 3, 16, 5, 6) :

| CODE |

MEANING |

EXAMPLE |

%Y |

Year with century as a decimal number |

2001 |

%y |

Year without century as a zero-padded decimal number |

01 |

%m |

Month as a zero-padded decimal number |

02 |

%B |

Month as locale’s full name |

February |

%b |

Month as locale’s abbreviated name |

Feb |

%d |

Day of the month as a zero-padded decimal number |

03 |

%A |

Weekday as locale’s full name |

Saturday |

%a |

Weekday as locale’s abbreviated name |

Sat |

%H |

Hour (24-hour clock) as a zero-padded decimal number |

16 |

%I |

Hour (12-hour clock) as a zero-padded decimal number |

04 |

%p |

Locale’s equivalent of either AM or PM |

PM |

%M |

Minute as a zero-padded decimal number |

05 |

%S |

Second as a zero-padded decimal number |

06 |

| CODE |

MEANING |

EXAMPLE |

%#m |

Month as a decimal number. (Windows) |

2 |

%-m |

Month as a decimal number. (Mac/Linux) |

2 |

%#x |

Long date |

Saturday, February 03, 2001 |

%#c |

Long date and time |

Saturday, February 03, 2001 16:05:06 |

from datetime import datetime

datetime(2001, 2, 3, 16, 5, 6).strftime("%A, %B %d, %Y %I:%M:%S %p")

result >>> 'Saturday, February 03, 2001 04:05:06 PM'

from matplotlib import dates

# TODO - find better example so i can use month or weekend formatter.

# using Date Locator's

#Miscellaneous

#Loops

# series

s = pd.Series(range(10000))

# list

l = list(s)

Panda’s Time Series

%timeit -n 1 -r 1 [s.iloc[i] for i in range(len(s))]

> 21.4 ms ± 0 ns per loop (mean ± std. dev. of 1 run, 1 loop each)

Python’s list

%timeit -n 1 -r 1 [l[i] for i in range(len(l))]

> 189 µs ± 0 ns per loop (mean ± std. dev. of 1 run, 1 loop each)

Pandas - accesing lst element

%timeit -n 1 -r 1 s.iloc[-1:]

> 53.8 µs ± 0 ns per loop (mean ± std. dev. of 1 run, 1 loop each)

List - accesing lst element

%timeit -n 1 -r 1 l[-1:]

> 375 ns ± 0 ns per loop (mean ± std. dev. of 1 run, 1 loop each)